Today I finally validated a decision I made more than five years ago — the 12/8/20 remix of my 401(k). I always felt the move was right, but I carried some doubt because parts of the portfolio lagged at times. Running the numbers now, I can see clearly why the decision worked and what it actually accomplished.

This wasn’t just a portfolio tweak.

It was a structural shift that changed the trajectory of my returns.

What I Actually Had Before the Change

Before the remix, my 401(k) was effectively split between:

- ~30% in the S&P 500 (from a prior rollover)

- ~70% in the Vanguard Target Retirement 2035 Fund

At the same time, all new contributions were being directed into VTTHX, which meant:

- Bond exposure would gradually increase

- The portfolio would become more conservative over time

- The allocation was drifting further away from my intent

This setup was simple—but increasingly misaligned with how I wanted my portfolio to behave.

What I Actually Did in December 2020

Looking back, I made two high-impact changes — and both mattered more than I realized at the time.

1. I removed automatic bond drag

Leaving Vanguard Target Retirement 2035 Fund meant stepping away from:

- ~30–35% bonds

- A forced glide path that would increase bond exposure over time

- No flexibility

That bond allocation wasn’t just protection — it had become a constraint on compounding.

Removing that drag was likely the single biggest contributor to my outperformance.

2. I built a new, intentional portfolio — with clear categories and purpose

Here is the allocation I created after the remix:

🔹 Large Cap (Core Engine) — ~51%

- S&P 500

- Tech-tilted OTC fund

🔹 International Equity — ~22%

- Total International Index

- EuroPacific

🔹 Small & Mid Cap — ~15%

- Extended Market

- Explorer (small cap)

🔹 Bonds — ~12%

- Total Bond Market

This was controlled concentration:

- Strong core in U.S. large cap

- A tech tilt to capture the cycle

- Diversifiers sized small enough not to hurt

- A modest bond slice for stability

That balance is why the portfolio behaved so well.

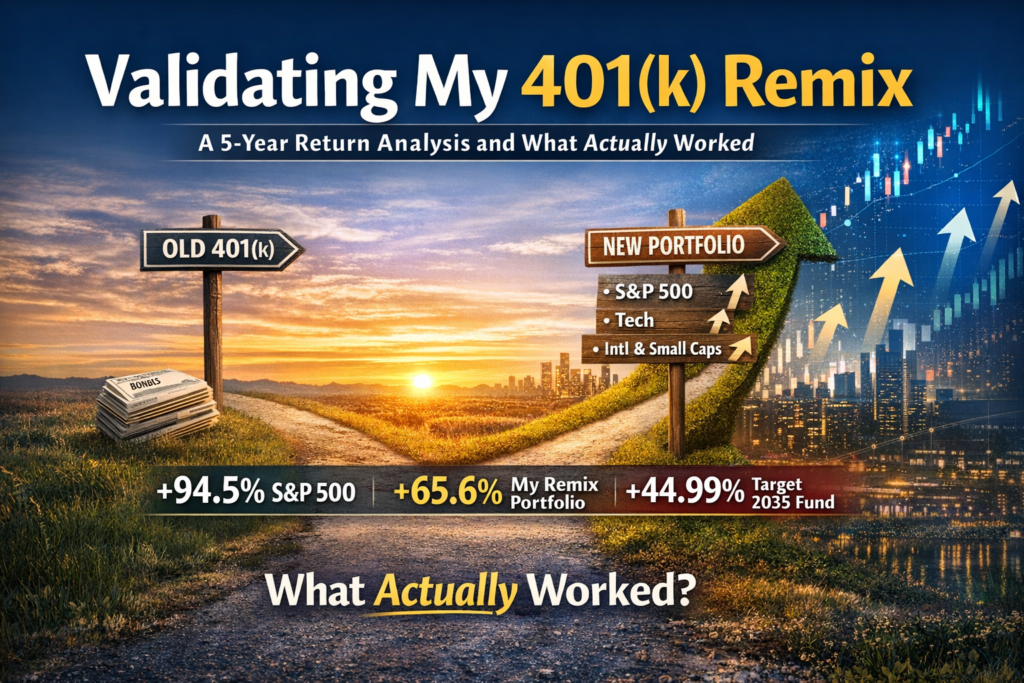

Return Comparison: Before vs. After the Change

This is the part that finally gave me full clarity.

Total Return (Dec 2020 → Mar 2026)

| Investment | Total Return | Annualized |

|---|---|---|

| S&P 500 (SPY) | +94.45% | 12.95%/yr |

| VTTHX (Target 2035) | +44.99% | 6.32%/yr |

| My Remix Portfolio | ~+65.6% | ~10.0%/yr |

Interpretation

- Staying in VTTHX would have meant 6.32%/yr

- A blended 30/70 S&P 500 / VTTHX mix would have been ~9.0%/yr

- My actual portfolio earned ~10.0%/yr

That extra ~1% per year compounded into a meaningful and measurable advantage over time — equivalent to roughly an additional 8% of the original portfolio value, even before accounting for contributions.

This is the clean mathematical validation of my decision.

What Really Drove the Outperformance

Primary contributors:

- Lower bond allocation

Bonds were historically weak from 2021–2023. I avoided that drag. - Large-cap U.S. dominance

The S&P 500 outperformed most other segments, and my allocation reflected that. - Tech concentration

The mega-cap cycle (AI, cloud, semiconductors) supported my tilt. - Letting winners run

I didn’t rebalance aggressively. That helped more than people realize.

What didn’t drive returns

- Small caps

- International equities (including EuroPacific)

- Bonds

These lagged — but my sizing kept them from meaningfully impacting the outcome.

A Subtle Insight: I Accidentally Built a Barbell

My portfolio ended up behaving like a barbell:

- Core (S&P 500 + tech) → growth engine

- Diversifiers (intl, small, bonds) → stability

Even though the diversifiers underperformed, they reduced volatility and made it easier to stay invested. That emotional stability was part of why the system worked.

Comparing This to My Roth Conversion Strategy

My Roth portfolio follows a different philosophy:

- Vanguard Total Stock Market ETF

- Avantis U.S. Small Cap Value ETF

- Avantis International Equity ETF

401(k) = cycle capture

- U.S. large-cap dominance

- Tech leadership

- Momentum-driven

Roth = factor + valuation capture

- Small/value tilt

- International exposure

- Mean reversion over time

They win in different environments.

The Big System Insight

Without planning it, I built a two-engine portfolio:

Engine 1 — 401(k)

- Momentum

- U.S. dominance

- Tech cycle

- Low bond drag

Engine 2 — Roth

- Small/value premium

- International valuation advantage

- Long-term mean reversion

- Tax-free compounding

These engines outperform at different times.

That means I’m not dependent on a single market regime.

One Honest Check-In

The 401(k) remix is fully validated by real performance.

The Roth strategy is still early. Recent outperformance from Avantis U.S. Small Cap Value ETF and Avantis International Equity ETF is encouraging, but factor strategies typically require full cycles (5–15 years) to fully play out.

A Final Note on Behavior

One thing this analysis doesn’t fully capture is behavior. The portfolio didn’t just work because of how it was built—it worked because I was able to stay with it when parts of it temporarily looked wrong. During the 2021–2022 drawdown and the volatility in 2025, there were moments when certain allocations lagged or felt out of sync. But the overall structure still made sense, and that made it possible to stay invested. In the end, the outcome reflects not just allocation decisions, but the ability to follow through on them when it mattered.

Takeaway

What I did right:

- Removed structural drift

- Reduced bond drag

- Maintained a strong equity core

- Let winners compound

- Built a second, differentiated engine

- Stayed invested through volatility and doubt

Final Result

A clear performance advantage —

amounting to roughly 8% additional value relative to the original portfolio baseline,

alongside a system I was able to follow in real conditions, not just on paper.