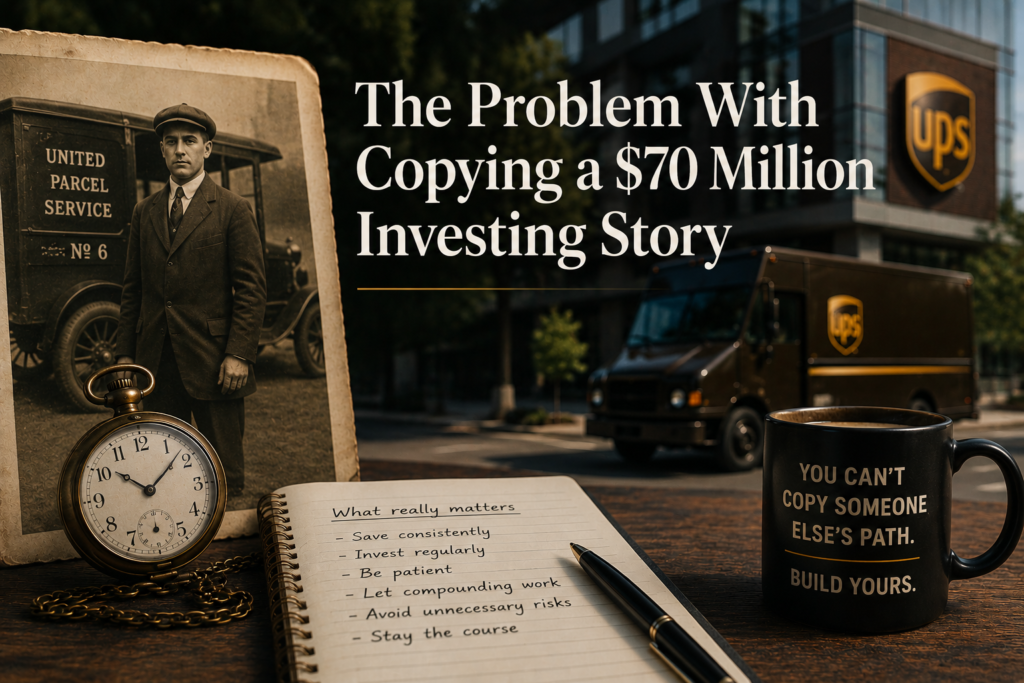

Every few years, the same investing story resurfaces. A UPS employee, Theodore Johnson, is said to have died with $70 million after holding company stock for decades. The details shift depending on who tells it, but the message people take away is usually the same: find one great company, hold it long enough, and compounding will take care of the rest.

I understand why this story resonates. It’s quiet, patient, and feels accessible in a way that trading or speculation does not. It suggests that wealth is built slowly, almost gently, through consistency rather than brilliance. I like that idea too. But the more I think about this story, the more I feel that the lesson most people take from it is incomplete. The story is not really about UPS, and it is not really about dividends. It is about something much harder to copy: the path.

Johnson joined UPS in 1924, long before it became the global company we know today. He wasn’t buying shares through a brokerage account or chasing yield. He was part of a small, growing company during a time when its future was still uncertain. Over the years, he accumulated stock and held it through decades of expansion, eventually retiring with a meaningful stake that continued to grow long after he stopped working.

What matters here is not just that he held the stock, but where he started. He owned a piece of a company that was still early in its growth, and he held it as it scaled into something much larger. That kind of transformation is rare, and it is tied to a specific period in history. Trying to recreate the outcome by buying the same company today misses that context entirely.

UPS today is a mature, global logistics business. It is stable, widely followed, and priced with decades of information already reflected in it. That doesn’t make it a bad investment, but it is no longer a small, underappreciated company quietly compounding inside a private environment. The conditions that allowed Johnson’s wealth to grow in that particular way simply no longer exist.

This is where many investing stories become misleading, even when they are factually correct. They compress decades of uncertainty into a neat narrative and present the ending as if it were always within reach. When we look at the final number, it’s easy to believe the path was obvious, or at least repeatable. In reality, the path depended on timing, environment, and a long series of decisions that could easily have gone the other way.

There is also the psychological side. Holding a single stock for decades sounds simple when we look backward, but it is not simple when you are living through it. Markets go through long stretches of doubt. Companies face setbacks, competition, and structural changes. There are always reasons to sell, especially after large gains or during difficult periods. Most people are not limited by their ability to find a good investment. They are limited by their ability to stay with a reasonable plan when it stops feeling easy.

This is why copying the visible part of the story does not lead to the same result. You can buy the stock. You can hold it. But you are not starting from the same place, and you are not moving through the same environment. The outcome belongs to that specific combination of circumstances, not just to the action of holding.

Over time, I’ve come to think that the more useful lesson is much simpler and much less dramatic. You don’t need a once‑in‑a‑lifetime stock to build wealth. What you need is consistency, patience, and the ability to avoid interrupting compounding. Saving steadily, investing regularly, and letting time do its work may not produce a dramatic story, but it is far more reliable.

It also fits better with how most of us actually live. We don’t have access to early private‑company equity in a future global giant. We don’t know which companies will dominate decades from now. What we do have is control over our savings rate, our spending, and our behavior over time. Those factors may not feel as powerful in the moment, but they compound in a way that is much more predictable.

When I read stories like this now, I still find them interesting, but I read them differently. Instead of asking how to repeat the exact outcome, I try to understand which parts of the behavior are transferable. Usually, that comes down to discipline, patience, and a willingness to stay the course even when nothing exciting seems to be happening.

The rest is not something we can copy. It belongs to a different time, a different company, and a different set of circumstances.

In the end, the problem is not the story itself. The problem is what we think it means.

In some ways, this reminds me of another investing illusion: the tendency to focus on billionaire outcomes while missing the deeper idea of independence and enoughness. I wrote more about that here:

Buffett, Munger, and the Billionaire Illusion: Why Independence Is the Real Prize